Healthcare costs in early retirement or self-employment are a high-stakes game. You have to pay attention today, and the wide variability means you also need to plan conservatively over the next few decades.

This is part one of a two part mini-series. Here I’ll answer the basic questions about how things work right now, so you can get comfortable estimating costs in the next year or two and know exactly how to get coverage if you leave your job. I’ll also show you how to estimate your income so you qualify for AGI/MAGI subsidies in 2026.

Part two can be found here, and takes on that nagging discomfort you may be feeling about whether healthcare costs over the next 20 to 30 years are a real threat to your wallet, and how to project your insurance and healthcare costs through an early retirement all the way to Medicare eligibility.

How to actually get coverage

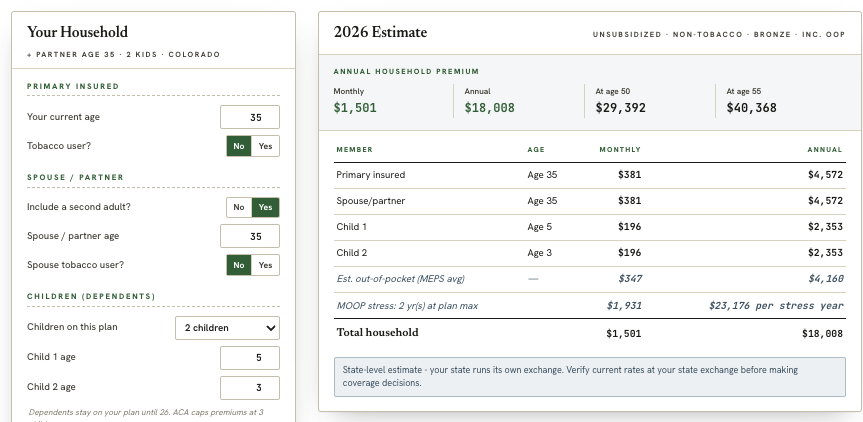

For self-employed workers who want a traditional insurance program, you shop plans at healthcare.gov. Or you can go to www.biggerpocketsmoney.com/healthcarecosts and use the tool I built, which gives an estimate (your number on healthcare.gov may vary) and projects costs at different ages and locations. For example, here is what my household in Colorado’s costs are estimated to be for a Bronze (high deductible) ACA compatible plan. If you want to use the too, click here.

On the surface, the mechanics of getting health insurance in early retirement or when self-employed are very straightforward. You quit your job. You go to healthcare.gov. You browse plans. You purchase one. You have insurance.

The Affordable Care Act imposes certain requirements on insurance plans. Insurers can’t price plans differently for people with pre-existing conditions. They can charge older Americans more (age is the number one correlate to healthcare spend), and in most states they can charge more if you smoke.

Some people reading this may be healthy, able-bodied, and building real wealth. For that cohort, the large majority will pick a Bronze ACA plan. Bronze plans come with the lowest monthly premiums but the largest out-of-pocket maximums and deductibles. That makes perfect sense for those pursuing financial independence – over long periods of time, the odds are almost by definition on the side of higher-deductible, lower-premium plans for the healthy and able-bodied. The tool at www.biggerpocketsmoney.com/healthcarecosts defaults to a Bronze plan and a family of four in Colorado.

How insurance is priced, and why location matters so much

When you shop for an ACA plan, depending on where you live, you may be shocked at the price in either direction.

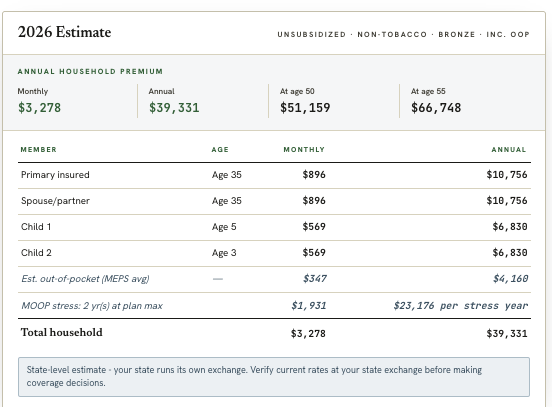

If I moved to Vermont, unsubsidized premiums run over $35,000 for a family of four, on average. If I moved to New Hampshire, that same coverage costs just over $10,000. For a lot of people, that’s a pleasant surprise – they’ve watched an employer pay far more for the same coverage for them and their families.

2026 Unsubsidized Healthcare Cost Estimate, Trench Household, Based in Vermont:

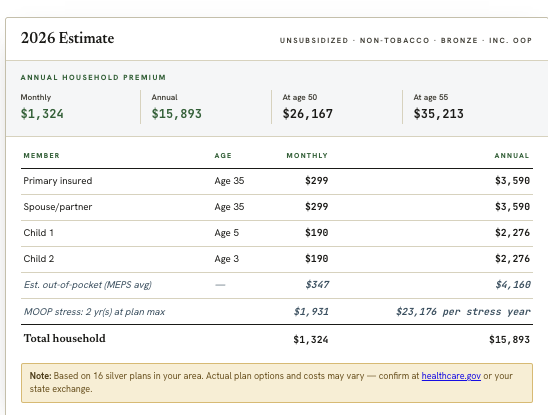

2026 Unsubsidized Healthcare Cost Estimate, Trench Household, Based in New Hampshire:

Yes, the differences are literally that extreme. The reasons are complicated, but they boil down to how each state allows for and handles competition on the exchange, local healthcare costs, and state regulations and risk pools. Vermont and New York tend to produce huge sticker shock, in part because they don’t allow insurers to charge different premiums based on age (the reason you see total healthcare costs rising by age 55 is because my tool assumes that out of pocket expenses rise with age, which I believe to be responsible projection modeling – I will discuss modeling healthcare costs as one ages in Part 2).

So the first step is to shop plans and understand what coverage is likely to cost in your area, or the area you plan to live in after you leave your job, with your current information. Basic geo-arbitrage can make an enormous difference in unsubsidized health insurance costs.

How subsidies come into play (It’s Very Weird)

Many people who leave their jobs won’t actually pay the full unsubsidized cost. And, the subsidy calculations are… weird. They may confuse you if you are new to this, or make you angry at the perverse incentives they create.

If you keep your MAGI (Modified Adjusted Gross Income) below 400% of the Federal Poverty Line (which varies by household size), you’re eligible for Premium Tax Credits. These directly offset your tax bill, and if the credit is greater than your tax bill, the rest is refunded to you – even if you owe no tax at all.

And, because the premium tax credit is based on the benchmark SILVER plan (comes with a lower deductible and out of pocket max than the bronze plan), you get strange effects.

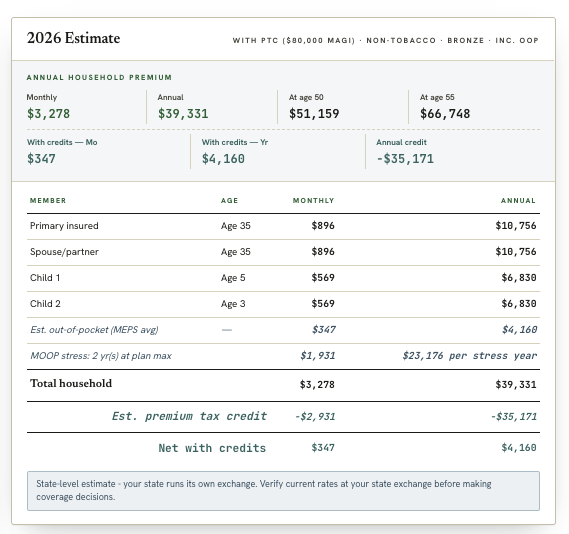

Remember that nearly $35,000 premium in Vermont? Well, the SILVER plan premiums for a family of four come out to nearly $50,000 annually. So, if I choose a bronze plan that *only* costs $35,000, and hadincome well below the MAGI cliff (more on this in a moment), I’d actually get the entire premium refunded to me via tax credits, effectively making health insurance free for my family in 2026.

2026 Subsidized Healthcare Cost Estimate, Trench Household, Based in Vermont:

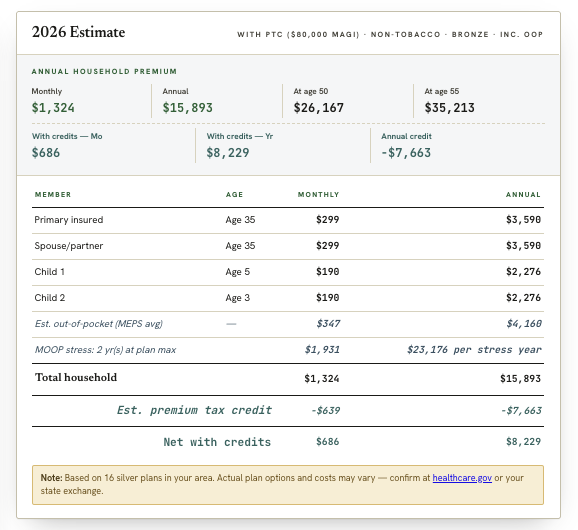

Remember that New Hampshire plan? That cost just under $12,000? Well, because the silver benchmark plan is so much cheaper, my family, in this example, would actually only get about $7,663 in Premium Tax Credits (with MAGI at $80,000 in this example). I’d be out of pocket for ~$5,000.

2026 Subsidized Healthcare Cost Estimate, Trench Household, Based in New Hampshire:

This is weird.

The takeaway is that, in practice, many families who keep their MAGI below the 400% of the Federal Poverty line may actually spend less on healthcare in the first few years after leaving a job than they did on their employer plan – as long as they stay eligible for Premium Tax Credits. Managed carefully, health insurance can be a very manageable expense.

Managing MAGI

Because of this, keeping MAGI below the 400% of the Federal Poverty Line is, in 2026, the single most important planning challenge for the self-employed and early retirees.

Go a dollar over and you get hit with a huge premium bill. So every other reason to realize income – Roth conversions, side hustles, realizing capital gains up to certain bracket thresholds – has to be managed and optimized under the constraint of not exceeding 400% of the Federal Poverty Line.

These rules are subject to constant revision. As of this writing in June 2026, the law imposes a cliff for MAGI over 400% of the Federal Poverty Line. That could change later this year or next.

What is MAGI?

MAGI is Modified Adjusted Gross Income, a modifier of Adjusted Gross Income.

Adjusted Gross Income is total income minus certain adjustments, and it’s the number that drives most phase-outs. It includes earned income, investment income, retirement and government benefits, and most other types of income. From that you subtract things like retirement contributions, HSA contributions, and self-employment taxes. If you’re self-employed, you also subtract your own health insurance premiums against your self-employment income. Sorry, early retirees – you can’t offset MAGI with premiums, though you do have options if you’re itemizing your deductions.

MAGI then takes AGI and modifies it further. Note that there’s MAGI in general, and ACA-specific MAGI. For ACA subsidies, you take AGI and add back tax-exempt interest (like municipal bonds), untaxed foreign income, and the non-taxable portion of Social Security.

In practice, most people will find their AGI and their ACA MAGI are the same. But the stakes are high if you’re an exception.

I built another tool at www.biggerpocketsmoney.com/income-tax-projection to help with this estimate. It’s an estimate, not a substitute for professional advice. But I think you’ll find it educational to watch how various income streams stack up and add to AGI and to see how the 400% of the Federal Poverty Line is computed.

Note that if you have the edge case income that is added back to MAGI, like tax-exempt interest like municipal bonds, untaxed foreign income, and social security, the tool will not adjust for those at the time of this publication.

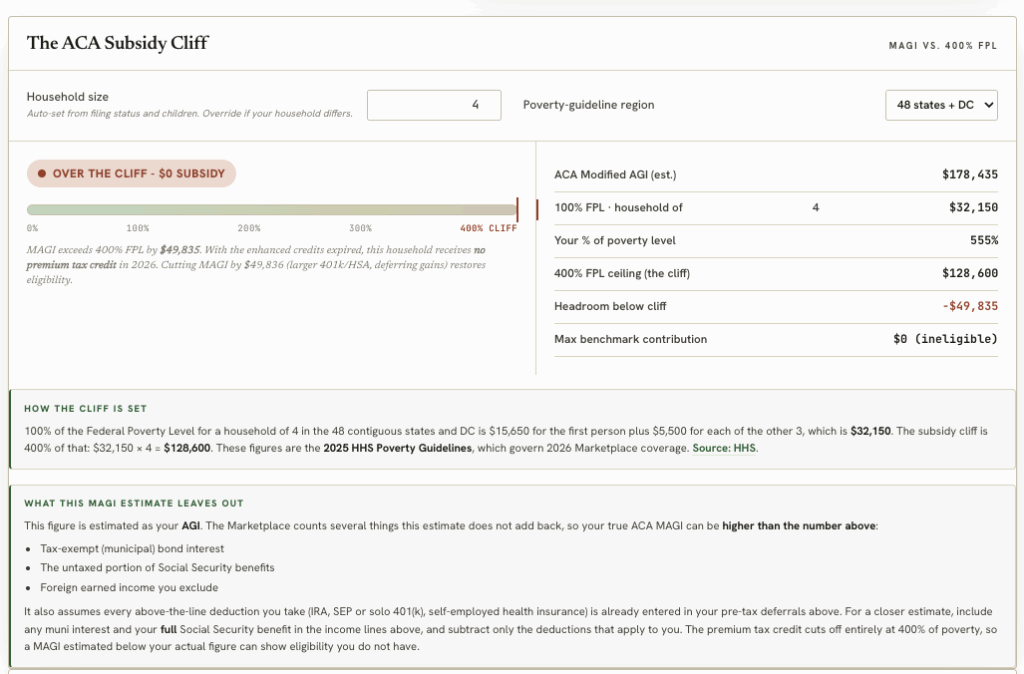

Illustrative Example of ACA Subsidy Cliff: Family of Four, Continental United States, $178K AGI:

A MAGI planning framework for 2026 to get you started

In practice, an early retiree or self-employed household that wants to be highly confident of not running over the MAGI limit should be careful about how it realizes income.

Some income just “happens” as a result of keeping your portfolio in place – qualified dividends, simple interest from the emergency fund in your high-yield savings account, rental income. Other income is a choice: to sell, to rebalance, to do Roth conversions, or to take early IRA withdrawals.

The safest play is usually to project the known sources of income, stay well below the AGI/MAGI threshold through the year, and then do a conservative end-of-year realization that approaches 400% of the Federal Poverty Line with a large cushion. And remember that many Bronze ACA plans are HSA-compatible, and HSA contributions reduce MAGI. That’s an easy, obvious win in any year you’re managing income to stay under 400% of the Federal Poverty Line.

Projecting income like this is a real challenge, which is why I built the income tax projection tool. Again, it’s not a substitute for professional advice, but it’s useful for a quick projection to see whether you have a meaningful margin of safety. You put in your various income sources and it gives an imperfect estimate of AGI/MAGI. There are traps: municipal/tax-free interest, foreign earned income, and Social Security all get added back to MAGI, and you want to enter your gross pay, not Box 1 of your W-2, if you’re employed.

Also, in another quirk – managing MAGI to such an extreme that you go below 100% of the Federal Poverty Line and you can also lose PTC eligibility and get routed to Medicaid.

Recap

- Mechanically, getting insurance is straightforward. Go to healthcare.gov and shop policies.

- Location is the single biggest variable in healthcare costs. The state and county you live in can make an enormous difference in your unsubsidized premiums.

- Premium Tax Credits make healthcare extremely manageable for most able-bodied self-employed and early-retiree households that keep MAGI below 400% of the Federal Poverty Line.

- Keeping MAGI under 400% of the Federal Poverty Line becomes the biggest planning constraint for early retirees, and it requires a detailed understanding of your tax projection for the calendar year.

In part two, I’ll cover how to model healthcare costs over the long haul of a FIRE journey. That’s a different problem from getting through the next year, and requires an opinion, and humility about the known unknowns.

Leave a Reply