This is Part 2 of a two part series for early retirees and self-employed households and health insurance. In Part 1 I covered how health insurance works for early retirees and the self-employed in 2026: how to get coverage, why location swings the price so much, how Premium Tax Credits work, and why staying under the MAGI cliff (keeping MAGI below 400% of the Federal Poverty Line to remain eligible for Premium Tax Credits) is, for now, the biggest planning constraint for early retirees, or those able to control their income in 2026.

If that’s how to think about a year of coverage, the next question is how to plan for this over the next few decades.

Three problems with long-term healthcare planning

- Healthcare costs are inherently variable. A typical healthy household can go years without needing meaningful care.

- Insurance premiums are almost certain to rise drastically over the next few years, absent reform or a collapse of the current system…

- …Reform, or collapse and rebirth of the current system, is a probable outcome over the next decade.

Here’s how I handle all three:

- Model healthcare costs as a base-case projection under current law, with conservative estimates.

- Take Premium Tax Credits while they’re available.

- Build a plan that survives both a continuation of the current model with rapidly rising base premiums, and the elimination or reform of Premium Tax Credits.

- Get and stay healthy (FitFI)

Your premiums will rise as you age, and that’s not inflation

Even without underlying healthcare inflation, your unsubsidized premiums are essentially certain to rise as you age. The ACA explicitly lets insurers charge older Americans up to 3x what they charge younger ones.

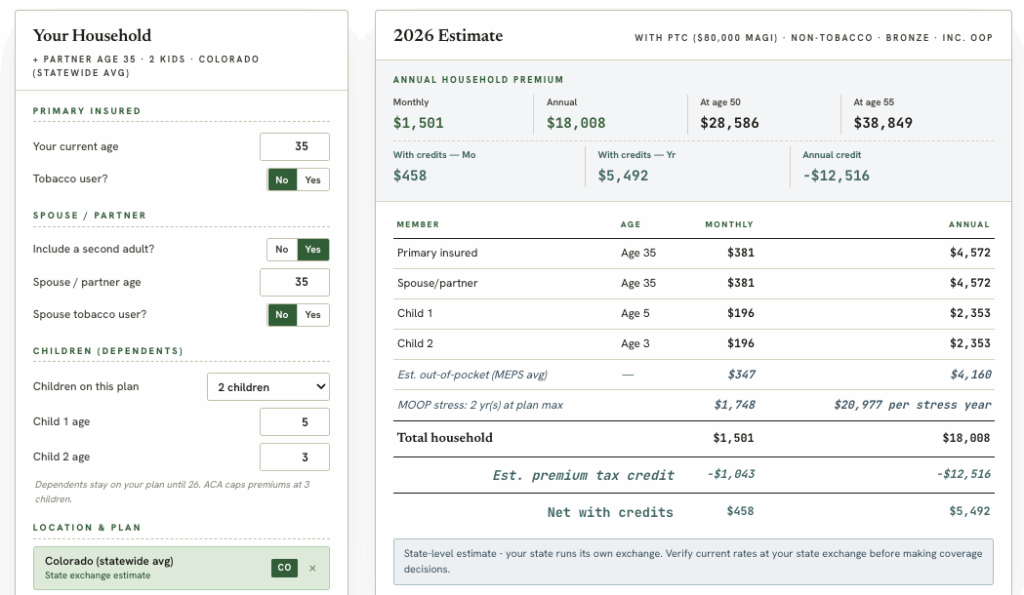

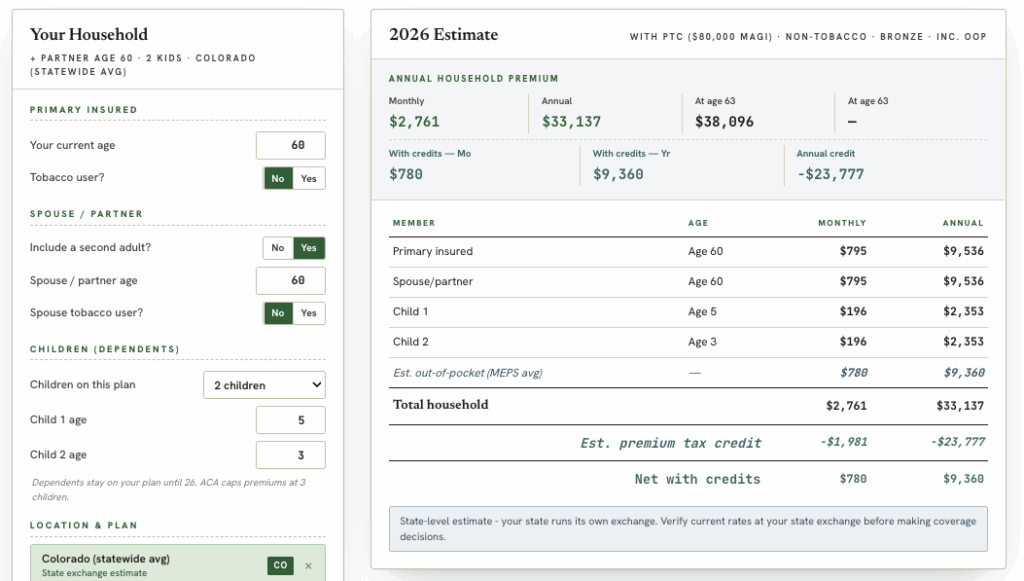

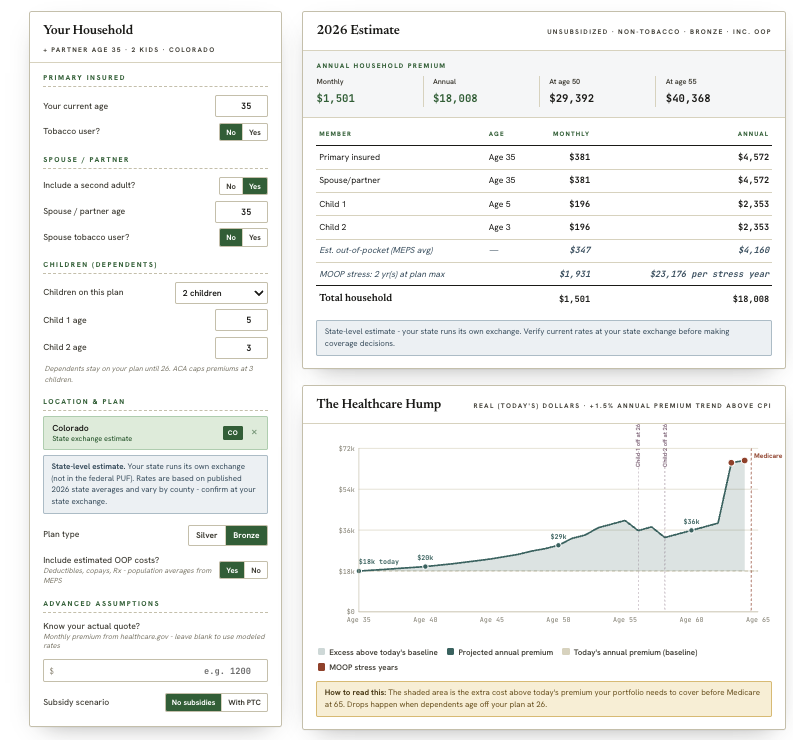

I don’t have to do anything fancy to project this. I can just shop plans and watch the price change with my age. Hold everything else constant and shop 2026 coverage as a 25-year-old in Colorado, and I’ll see premiums around $310 a month. Shop the same year as a 64-year-old in Colorado, and it’s $926 a month.

I also built a free tool over at www.biggerpocketsmoney.com/healthcarecosts to help with estimating insuranace costs. You can see that, before we even get to healthcare inflation (more on this in a moment), my premium costs will rise drastically as I age:

Unsubsidized Healthcare Costs Estimate, Trench Family, Age 35, Colorado

Unsubsidized Healthcare Costs Estimate, Trench Family, Age 60, Colorado

That’s not inflation. That’s just the cost rising as I age.

It’s the law, and the insurance marketplace, operating as explicitly designed.

Your Out of Pocket Costs Will Increase As You Age… And That is Also Not Inflation

The reason that insurers charge more for insurance premiums as we age is that age is the number one correlate to healthcare spending. This is not inflation as measured by CPI. It’s the reality of our biology. As a 35 year old, I cannot take a baseline of my healthcare spend, out of pocket, over the last 10 years, and use that to project my out of pocket healthcare spending for the next 30 years. These costs are going to go up. Unless I explicitly plan for other parts of my spending to come down to offset this, I need to plan for these expenses to rise on average, in addition to my premiums going up, to responsibly model out costs over an early retirement or life of self-employment.

Again – that is not healthcare inflation. I do not get a say in this cost increase. I will get older, and I will spend more on both healthcare premiums, and out of pocket expenses, assuming zero inflation.

Why it’s a bad plan to rely on Premium Tax Credits

Premium Tax Credits refund premium costs to households below 400% of the Federal Poverty Line. They’re designed to subsidize low-income families. They aren’t designed to subsidize millionaire early-retiree households. We discussed how to manage eligibility for these subsidies in great detail in Part 1 of this series.

No one’s arguing against taking the benefits and deductions you’re owed under the current rules. But it’s a bad, silly plan to assume that someone who retires in their 30s or 40s with millions in assets will collect low-income subsidies for decades. That’s an irresponsible, specific political bet. We won’t model it at BiggerPockets Money, even as we DO attempt to model how to manage income to remain eligible for them under the current law.

What we will model is the unsubsidized cost of insurance, in a given geography, under today’s rules – knowing the most likely base case is for that to continue, probably rising much faster than inflation (NOW I am talking about inflation) for the next few years, before some new wrinkle, technological or legislative, changes the projection down the road. And we can do that easily, with publicly available datasets.

Why Aggregate US Healthcare Costs Are Overwhelmingly Likely to Rise Faster than Inflation

Again. NOW we are talking about inflation for healthcare costs.

The defining feature of the ACA is that it legislates exactly which risks insurers can and can’t charge for. The two that matter most here: insurers can’t charge higher premiums for people with existing conditions, and they can charge higher premiums based on age.

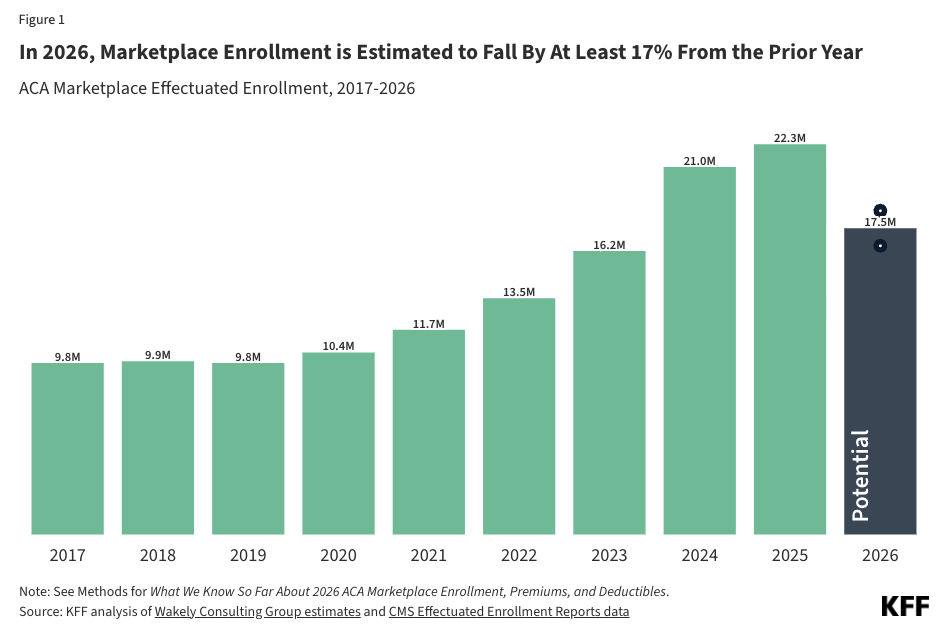

When the ACA first passed, there was a controversial penalty on anyone who didn’t carry insurance. The logic was simple – if everyone pays premiums, the premium per person goes down. The 2017 Tax Cuts and Jobs Act eliminated that penalty, effective 2019, and people began leaving the insured pool. Most of those departures came from people who weren’t receiving subsidies, especially on plans not eligible for Premium Tax Credits.

Then the pandemic hit, and the uninsured pool dropped sharply as Congress passed emergency provisions. But over the last few years the uninsured pool has been rising again, and in 2026 it’s expected to accelerate.

During COVID, enhanced federal tax credits made it appealing for high-income people to get ACA coverage and still receive subsidies. Those enhanced credits expired at the end of 2025. In 2026, if your MAGI is over 400% of the Federal Poverty Line, you get no Premium Tax Credits at all. Millions of people are now doing the hard math on whether to self-insure, go with an alternative like a healthshare, or just eat the premium. Some fraction are choosing alternatives to the ACA.

Here’s what this pattern looks like:

Healthshares, by the way, are an increasingly serious option in the self-employed and early-retirement worlds. They use different terminology than insurance – they “share” healthcare costs rather than “insure” them – often have lifestyle or religious eligibility requirements, and usually don’t share costs for pre-existing conditions. They have real pros and cons, but expect their share to keep growing until the underlying problems with American health insurance get addressed.

This exodus from ACA insurance products creates a nasty circularity. Underlying healthcare costs are already rising in the U.S. as the population ages. But premiums are rising even faster than underlying costs, in part because healthy people are leaving the traditionally insured pool. Until that’s fixed, I expect more healthy Americans who don’t qualify for Premium Tax Credits to leave the pool, which leaves the remaining insured pool disproportionately less healthy, which drives premiums up faster still.

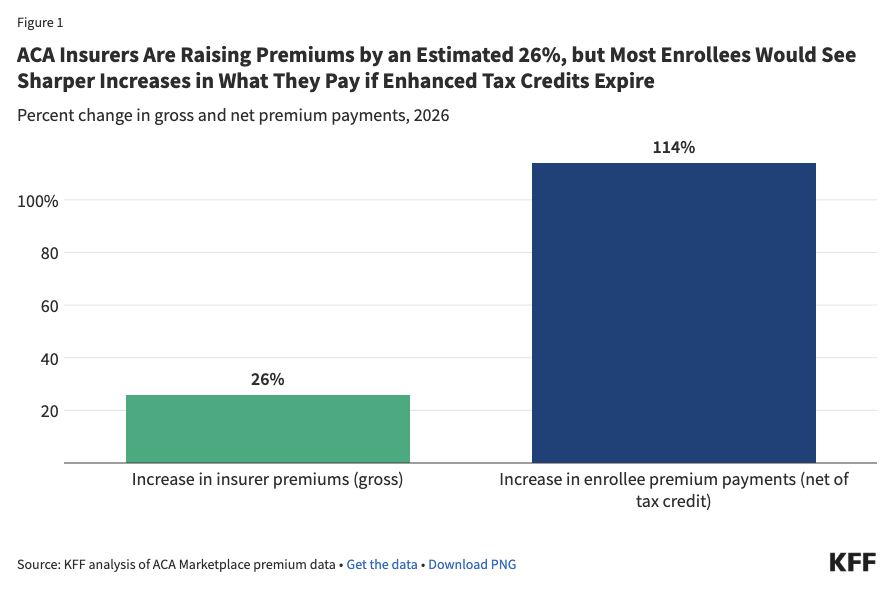

In 2026, insurance premiums skyrocketed by 26% on average for ACA plans, and because of the MAGI cliff I discussed at length in part 1, the net premium payments made by ACA participants more than doubled on average.

It does not take a detailed projection model to guess what will happen in 2027 without legislative or technological change. Of the remaining population, more and more of those in good health will drop from the ACA marketplace, either because the insurance is so expensive that it is overwhelmingly better value to self insure or find alternatives like the before-mentioned healthsares (despite the discomfort and real risk), or because they will simply be unable to afford the payments.

I’m optimistic that technological or legislative breakthroughs, AI, and rising health awareness in America could cut these costs substantially in the coming decades. But so far, not so good. And, I won’t count on it in 2026 or 2027.

Until we see it, I think it’s irresponsible to plan as if these costs won’t rise, on average, faster than the rest of CPI – even as other costs that make up CPI potentially come down.

How to model this

Here’s how I decided to model healthcare costs for myself, and how the tool I built works:

- Enter your age, your spouse’s age, and your children’s ages, if applicable.

- Enter your plan type (it defaults to Bronze).

- Enter your MAGI.

- If you have a real quote, use that instead of the calculator’s estimate.

- The calculator shows its work for your 2026 insurance quote estimate, and makes a defensible guess at your out-of-pocket expenses.

- It then applies the law to rising premiums, gradually increases your out-of-pocket costs, and lets you add a healthcare inflation adjustment above CPI if you want one.

- Optionally, add “stress test” years that assume an occasional health event requiring a maximum out-of-pocket outlay. Set it to zero or to five. If you think you’ll have more than five such years, you might want a different plan type or approach to insurance altogether.

The point of all this is to project healthcare costs as a bridge to Medicare, where costs drop sharply.

Medicare is a whole separate debate. For now, I’m limiting the analysis to the understudied area of ACA insurance in early retirement and self-employment, which I’ve studied in much more depth than Medicare sustainability. I’ll leave that one for the comments.

The “Healthcare Hump” for my family of four in Colorado:

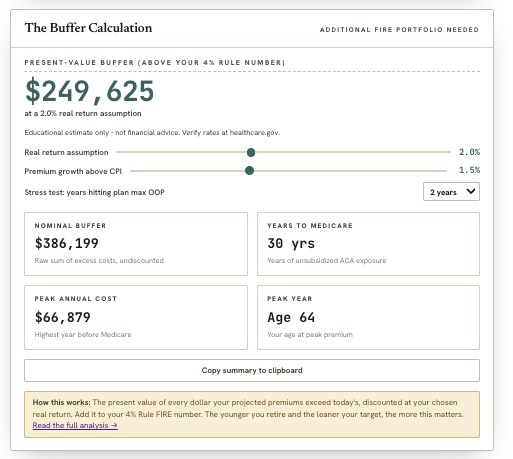

The area under the curve (yes, calculus) is the amount that I have to fund in excess of traditional retirement planning. Traditional rules of thumb, like the 4% rule, assume constant, inflation adjusted spending. But, at least a portion of healthcare spending is NOT INFLATION. We must account for that separately to responsibly project spending.

My method for accounting for this is to do a present value calculation. I default to slightly higher than CPI inflation in healthcare spend (this is debatable – so it is an input), and also model the rise in premium costs as I age (this is not debatable under current law, so it’s not an option for me or you to toggle in the tool. I also default to assuming that in two years out of the next 30, some problem will come up that will force me to use my entire Out of Pocket Maximum (the tool allows you to make an assumption for this as well).

This gives me a present value calculation for the cost of healthcare over and above my current year’s spending.

Depending on my return assumption (I assume 2% real), this is the amount over and above my traditionally planned FI number using a 4% withdrawal rate that I need to plan for to cover healthcare costs. I estimate my buffer at about an extra $250,000, personally, for my family, in Colorado.

Again, at age 65, I assume medicare eligibility and a steep drop off in healthcare expenses.

What to do today

If you’ve made it this far, you might be thinking “so what?” Here’s what you can do right now to get a handle on your healthcare costs:

- Check out the health insurance projection tool at www.biggerpocketsmoney.com/healthcarecosts to see what your situation could look like, and how geolocation plays a role if relocating is on the table.

- Check out the tax projection tool at www.biggerpocketsmoney.com/income-tax-projection to play with the inputs and see how your choices move your Adjusted Gross Income and MAGI.

- Consider talking to a health insurance broker. They can help you weigh the pros and cons of an ACA plan versus a healthshare, and you pay the same rate whether you shop the exchange yourself or use a broker.

- If all of this is overwhelming and you’d rather not DIY it, or you’d like to talk to a CFP, we’re partnered with Domain Money, a flat-fee financial planning firm (no AUM fees, no product sales or commissions). We receive compensation if you work with them. Learn more at www.biggerpocketsmoney.com/CFP – and we encourage you to interview them as part of your process for finding a CFP.

Leave a Reply